Credit Card vs. Debit: Which is the Best Option for Your Personal Finances?

The Evolution of Payment Methods

Throughout history, the transformation of monetary systems has mirrored societal changes, technological advancements, and shifts in consumer behavior. The move from the ancient barter system, where goods and services were exchanged directly, to our current ecosystem of digital currencies highlights the intricacies of financial evolution. This journey is particularly evident in the Canadian landscape, where payment methods such as credit cards and debit cards dominate consumer transactions.

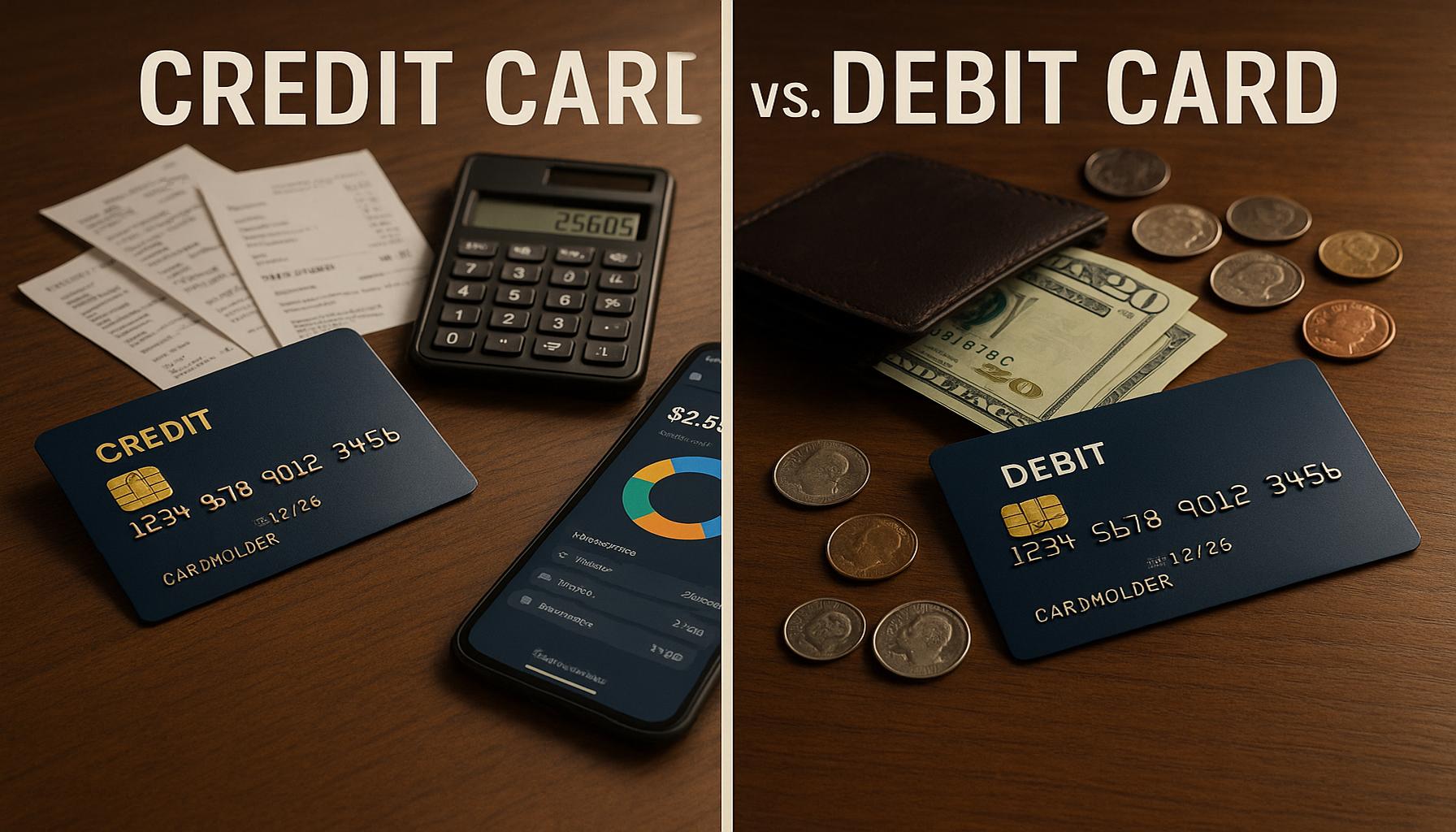

Examining credit cards, they have revolutionized the way individuals interact with money. In Canada, the appeal of credit cards often lies in their reward programs, which can promote consumer loyalty. For instance, many Canadians earn points that can be redeemed for travel, merchandise, or cash back through their purchases. Additionally, using credit cards responsibly can help individuals build a solid credit history, an essential factor for significant financial decisions like qualifying for a mortgage or securing lower interest rates on loans.

Conversely, debit cards present a no-frills approach to spending by allowing users to access funds directly from their bank accounts. This method inherentlysupports personal finance management, as it requires individuals to live within their means and avoid debt accumulation. The growing popularity of budgeting apps, often linked to debit card usage, showcases Canadians’ desire for financial accountability and awareness in a world fraught with impulsive spending.

The ramifications of historical events, such as the 2008 financial crisis, teach us valuable lessons about responsible financial behavior. This crisis underscored the perils of excessive borrowing and poor credit management, leaving lasting impressions on consumers. Canadians, in the years since, have become more cautious, opting for less risky financial strategies. Such shifts in attitude towards credit and debt management foster a more sustainable economic environment, as evidenced by the increased emphasis on financial literacy programs across the country.

As consumers navigate the landscape of financial choices today, understanding the implications of each payment method is paramount. The lessons learned from past economic crises continue to shape conversations about responsible financial practices, urging individuals to make well-informed decisions that safeguard their financial futures. Ultimately, these choices can cultivate a healthier financial ecosystem not only for individuals but for Canadian society as a whole.

DISCOVER MORE: Click here to learn how to apply for the Amex Aeroplan Card

The Pros and Cons of Credit Cards

Understanding the nuances of credit cards involves looking beyond mere convenience; it’s essential to weigh the associated benefits and drawbacks. The allure of credit cards lies primarily in their capacity to facilitate large purchases while granting consumers access to funds they may not currently possess. This aspect was particularly significant following the 2008 financial crisis, when many Canadians faced financial constraints and began utilizing credit cards as a means to maintain purchasing power without depleting their savings. With the right strategy, credit cards can offer significant advantages.

- Rewards and Incentives: Many credit cards provide rewards systems that allow users to earn points or cash back on their purchases. This feature encourages responsible spending and rewards individuals for using credit prudently.

- Building Credit History: Regular, timely payments on credit cards contribute positively to an individual’s credit score. A robust credit history is vital when applying for future loans or mortgages.

- Emergency Coverage: Credit cards offer a financial safety net in emergencies, allowing users to make essential purchases when they face short-term cash flow problems.

However, utilizing credit cards also carries inherent risks. Poor financial habits may lead to unmanageable debt, a lesson that has been ingrained into the psyche of many consumers since the above-mentioned financial crisis. With mounting high-interest rates and the temptation of easy credit, Canadians risk falling into cycles of debt if they fail to monitor their spending closely. Here are some prevalent drawbacks of credit cards:

- High-Interest Rates: Failing to pay off the full balance each month can result in significant interest charges, which can accumulate quickly.

- Potential for Overspending: The ability to spend money not currently available can encourage impulsive purchases, deviating from budgetary constraints.

- Debt Accumulation: If not managed properly, credit card debt can spiral out of control, impacting long-term financial stability.

A Closer Look at Debit Cards

On the opposite end of the spectrum, debit cards offer a more straightforward approach to personal finance, drawing funds directly from a linked bank account. This method aligns closely with a budgeting mindset that many Canadians have adopted since the financial turmoil of the late 2000s. Debit cards provide a sense of control, urging individuals to maintain spending within their existing means and effectively evade debt accumulation.

One significant advantage of debit cards is their simplicity. Users can track their spending in real-time, as transactions deduct directly from their bank accounts. This immediate reflection of spending can instill a sense of accountability that credit cards often lack. Furthermore, with budgeting apps gaining traction among Canadians, users can integrate their debit transactions seamlessly to monitor their finances accurately.

- Immediate Transactions: Since purchases deduct directly from a user’s bank account, there is no chance of overspending or accumulating debt.

- Lower Fees: Debit cards usually come with minimal fees compared to credit cards, making them an economical choice for everyday transactions.

- Encourages Saving: With debit cards, individuals are more likely to adhere to a budget, which can foster better saving habits for the future.

While debit cards present these advantages, they also have limitations that merit consideration. The absence of rewards programs and minimal protections against fraud can dissuade some users from opting for debit over credit. In the current landscape of personal finance, both payment options come with inherent pros and cons that users must evaluate in the context of their financial goals and spending behaviors.

DISCOVER MORE: Click here for the application guide

Evaluating the Risks and Benefits of Each Payment Method

In navigating the complexities of modern personal finance, it becomes clear that the selection between credit cards and debit cards is not merely a matter of preference but a pivotal decision influenced by historical precedents. The lessons gleaned from past economic upheavals, such as the dot-com bubble and the housing market crash, provide context for understanding how to wield these financial tools effectively. Drawing parallels between these events can shed light on the current landscape of credit and debit use.

Credit cards have seen an evolution not just in functionality, but also in usage patterns, particularly since the early 2000s. When consumers were encouraged to leverage credit for greater purchasing power, many, unfortunately, began to equate access to credit with financial stability. This misconception often led individuals down a treacherous path of debt accumulation, a situation exacerbated by predatory lending practices and enticing promotional offers that masqueraded as financial empowerment. Today, the memories of financial crisis still resonate, prompting individuals to re-evaluate their relationships with credit.

On the flip side, the pervasive use of debit cards offers a cautionary tale about underutilizing credit’s potential benefits. While debit cards encourage a more disciplined approach to spending, they may inadvertently perpetuate a cycle of underconsumption or restrict financial growth. Individuals who rely solely on debit may miss out on opportunities to build a robust credit profile, which is vital in a world where establishing a solid credit history is essential for accessing favorable financing options in the future. Thus, understanding the balance between using credit to enhance one’s financial portfolio and employing debit for fiscal responsibility becomes crucial.

- Financial Discipline: Utilizing debit cards often instills a habit of financial discipline, requiring users to adhere strictly to their available funds, thereby preventing debt. This practice resonates with the hard lessons learned during economic downturns when overreliance on credit can lead to financial ruin.

- Limiting Financial Exposure: The absence of credit limits and potential fees often makes debit cards a less risky option. During periods of economic uncertainty, consumers have turned to debit as a means to limit their financial exposure, embodying a more cautious approach overall.

- The Importance of Credit Education: In a world increasingly driven by credit, understanding how to leverage it effectively is paramount. Education around credit scores, interest rates, and benefits associated with responsible credit use has become vital in helping consumers avoid the pitfalls of the past.

Moreover, the advancements in technology and emerging financial tools, akin to the evolution experienced during earlier banking reforms, have facilitated a convergence of credit and debit functionalities. The rise of mobile wallets and prepaid cards offers consumers hybrid options that provide features of both credit and debit cards. Users can now blend convenience and control, suggesting a potential shift in how Canadians manage their personal finances while mitigating risk.

As one contemplates their financial strategy today, it is essential to consider not only one’s current lifestyle but also the historical context of financial decisions and their ramifications. Both credit and debit have their virtues and vices, and understanding these dynamics, alongside lessons from past financial upheavals, will enable individuals to make informed decisions conducive to their long-term financial health.

DISCOVER MORE: Click here to learn how to apply for the Amex SimplyCash Card</p

Drawing Conclusions: Making Informed Financial Choices

In the quest to determine the superior option between credit cards and debit cards, it becomes increasingly evident that one’s choice must reflect not only personal financial habits but also a profound understanding of historical context. As we have seen, the lessons from past economic crises reveal the potential dangers of excessive reliance on credit, prompting consumers to practice caution and discernment. Similarly, the disciplined approach facilitated by debit cards underscores the importance of living within one’s means, yet it also hints at the risks of foregoing credit opportunities that contribute to long-term financial growth.

As Canadians navigate the financial landscape today, they stand at a crossroads, armed with the insights gleaned from experiences past. The rise of innovative payment methods and a greater emphasis on credit education provide a new perspective—one where a harmonious blend of credit and debit usage can cultivate financial resilience. Such a strategy not only allows for more thorough fiscal management but also paves the way for a healthier credit profile that is crucial in an increasingly credit-driven society.

In conclusion, the selection of a payment method should not be a mere reflection of personal preference, but rather a calculated decision that weighs the lessons of history against contemporary financial realities. By fostering a balanced relationship with both credit and debit, individuals can equip themselves with the tools needed for robust financial health, enabling them to thrive in an era marked by both opportunity and uncertainty.

Linda Carter

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on our platform. Her goal is to empower readers with practical advice and strategies for financial success.