The Impact of Credit Card Interest Rates on the Financial Health of Canadians

The Evolution of Interest Rates in Canada

The financial landscape of Canada has undergone significant changes over the past few decades, deeply impacted by the fluctuating interest rates that have shaped Canadians’ financial choices. To appreciate today’s economic scenario, it is essential to trace the evolution of these rates and understand their historical context.

In the latter half of the 20th century, Canadians were grappling with economic challenges characterized by high inflation and exorbitant credit card interest rates. Throughout the 1980s, interest rates soared, reaching above 20% at one point, which turned credit into an expensive commodity. Many Canadians found themselves ensnared in debilitating debt, struggling to keep up with the relentless burden of monthly payments. By understanding this backdrop, we recognize that today’s challenges are not unprecedented but rather echoes of financial crises from the past.

Impact of Rising Interest Rates

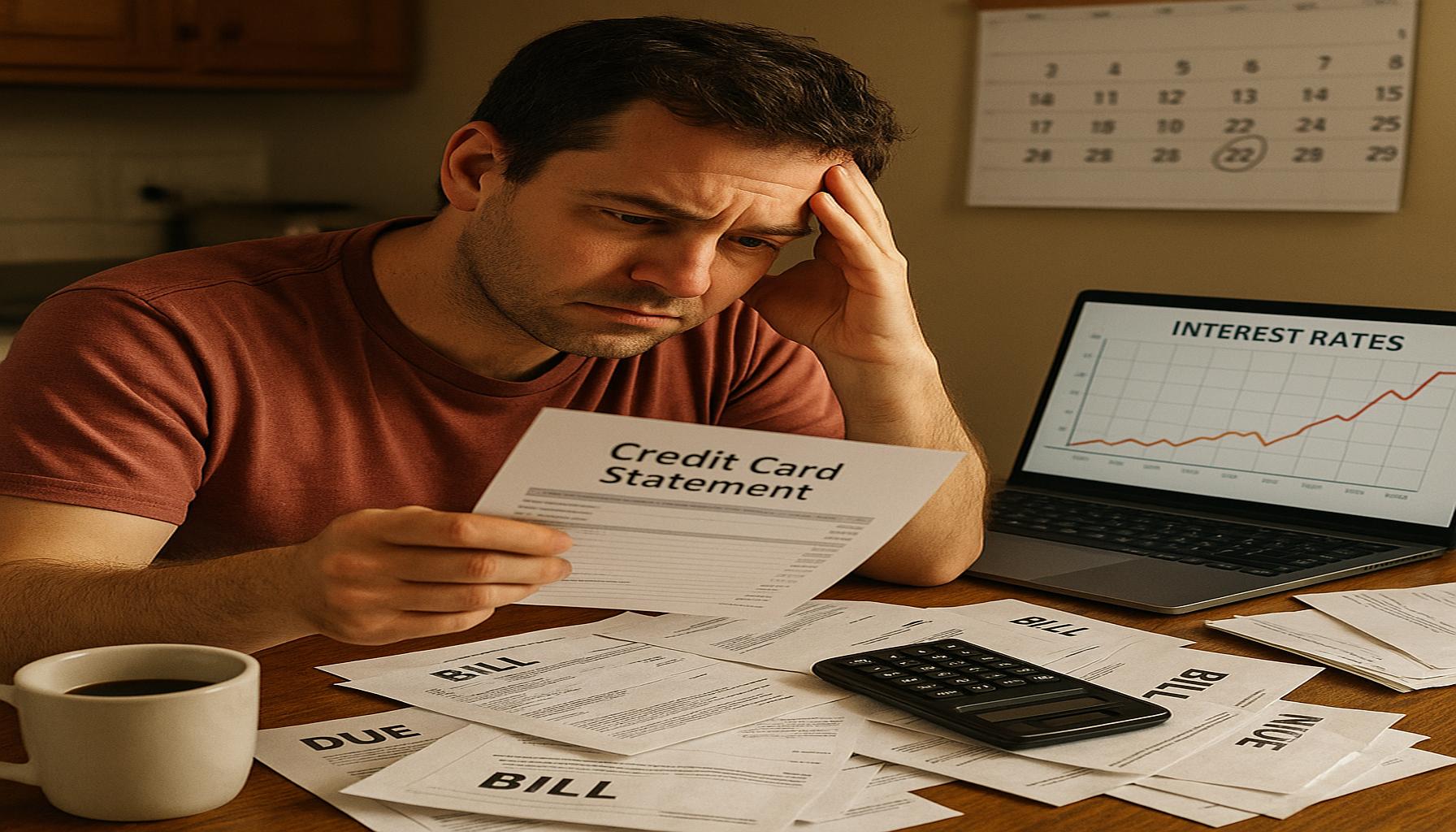

In recent years, interest rates have begun to rise again, marking a departure from the historically low rates that had characterized the decade following the 2008 financial crisis. As the Bank of Canada increases rates to combat inflation, borrowing costs rise across the board. This shift has profound consequences for consumers, as carrying a balance on credit cards becomes increasingly costly. For example, if a Canadian carries a balance of $5,000 on a credit card with an interest rate of 19.99%, the cost of maintaining that debt can exceed $1,000 in interest payments over the year. Such a financial strain can dissuade individuals from making purchases or can lead to further debt accumulation.

The Cycle of Debt Accumulation

Furthermore, as more Canadians find themselves in the cycle of borrowing, the landscape of personal finance becomes more precarious. Many individuals resort to credit to make ends meet, leading to mounting interest expenses that compound their financial woes. The Canadian financial landscape is increasingly littered with stories of individuals who, trapped in cycles of increasing debt, find it difficult to escape. The recent trend of personal bankruptcy filings serves as a stark reminder of the consequences of unresolved financial pressures.

The Importance of Financial Literacy

In light of these challenges, it is evident that financial literacy has emerged as a pivotal need that can no longer be overlooked. Today’s consumers must navigate an intricate web of products, promotions, and potential pitfalls within the credit landscape. Understanding how to manage credit wisely, including recognizing the implications of variable versus fixed rates, and utilizing tools such as budget planners, becomes imperative for anyone looking to achieve financial stability in this rising interest rate environment. Moreover, educational initiatives aimed at enhancing financial literacy have become crucial to empower Canadians to make informed decisions about their finances.

By examining the impact of credit card interest rates on personal financial health, we uncover essential patterns that are evident in Canada’s current fiscal environment. The lessons learned from past financial crises serve as valuable guides in navigating present challenges, suggesting that historical context plays a crucial role in shaping our responses to contemporary economic realities.

LEARN MORE: Click here for essential financial planning tips

Understanding the Historical Context

The fluctuations in credit card interest rates serve as a reminder of the cyclical nature of economic conditions in Canada. Looking back to the early 2000s, Canadians reveled in the era of accessible credit, with low interest rates encouraging spending and economic growth. This period of stability, however, was not without its pitfalls. The ease of borrowing, spurred by enticing credit card promotions and minimal interest rates, led many consumers to engage in reckless fiscal behavior, inadvertently setting the stage for future financial hardship.

As rates began their gradual ascent post-2008, the repercussions rippled through households across the nation. Many Canadians, who had relied on credit as a financial crutch during times of unemployment or economic downturn, suddenly faced an inhospitable landscape marked by rising interest rates. This scenario paints a vivid picture of how the past continues to influence the present—despite the apparent recovery, the ghosts of prior fiscal irresponsibility linger, dictating the financial choices of a cautious populace.

The Impact on Consumer Behavior

In a climate where interest rates are constantly shifting, consumer behavior reflects an oscillation between cautious spending and impulsive borrowing. The implications of rising interest rates can be observed in several key areas:

- Increased Minimum Payments: With higher interest rates, the minimum payments on credit card balances rise, leaving consumers with less disposable income.

- Decreased Spending Power: Strapped by the increasing cost of their existing debts, many Canadians may choose to curtail their spending, impacting overall economic growth.

- Rising Household Debt Levels: Some families may be compelled to open new credit lines to manage existing debts, perpetuating a cycle of dependence on borrowed funds.

The net effect of these changes has created a precarious financial balance for many households. As consumers allocate more of their income to servicing debt, they find themselves with diminished resources to invest in necessities or save for the future. This scenario starkly echoes the experience of previous generations who suffered during periods of economic tightening, laden with high interest rates that crippled their financial mobility.

The Lessons of History

The enduring lesson from past economic cycles remains remarkably relevant today: the importance of prudent financial management cannot be overstated. As Canadians navigate the current landscape marked by rising credit card interest rates, many have taken conscious steps to remedy their financial health. Whether through cutting non-essential expenditures or increased payments on outstanding balances, the initiative towards financial literacy and responsibility is beginning to gain traction.

Clearly, awareness of historical trends not only contextualizes the present economic climate but also fosters a sense of agency among consumers. The echoes of previous financial crises advocate for a more informed approach to credit usage, ultimately steering Canadians towards the pursuit of smarter financial practices and healthier economic futures.

DISCOVER MORE: Click here for detailed application steps

The Weight of Rising Debt

As Canadian households grapple with the specter of increasing credit card interest rates, the overall financial health of the nation stands at a critical juncture. Drawing parallels between the present-day scenario and historical economic downturns reveals essential insights into consumer sentiment and behavior. The late 1980s and early 1990s serve as striking examples, where high-interest burdens exacerbated economic strife, ultimately influencing borrowing behaviors that persisted long after the rates stabilized.

In analyzing the current situation, it becomes evident that a substantial number of Canadians are finding themselves ensnared in a web of mounting debt. Statistics Canada reported in 2022 that the average Canadian household debt reached a staggering $1.84 for every dollar of disposable income, a condition reminiscent of the fiscal crises faced in previous decades. As credit card rates rise, consumers may be compelled to service their high-interest debts first, prioritizing repayments to avoid penalties. The consequence is a formidable shift towards minimal financial flexibility, as what remains of their income is siphoned away to a growing avalanche of interest payments.

Navigating Financial Literacy

This prevailing atmosphere brings forth an urgent need for enhanced financial literacy among individuals. Historical missteps during times of economic zeal manifested as widespread ignorance regarding credit management, leading to substantial losses during downturns. Today, with an abundance of educational resources available through digital platforms and community workshops, Canadians have the opportunity to learn from the past to forge stronger financial futures. Understanding the intricacies of interest calculations and the significance of timely payments enables consumers to make informed choices that can ultimately mitigate the effects of rising rates.

- Credit Counselling Services: Many Canadians are beginning to seek assistance from non-profit organizations that provide credit counseling services, equipping individuals with strategies to manage their debts effectively.

- Debt Snowball Method: Among the strategies gaining traction is the debt snowball method, which encourages individuals to tackle smaller debts first, fostering a sense of accomplishment and motivation to eliminate debt more rapidly.

- Emphasis on Saving: Moreover, as a direct countermeasure against high-interest burdens, more Canadians are recognizing the importance of creating emergency funds to stave off reliance on credit cards for unforeseen expenses.

While the results of these financial literacy efforts will take time to manifest, the initial signs are promising. Consumers are increasingly opting for lower-interest loans in lieu of credit cards, indicative of a more cautious approach honed by lessons from the past. Furthermore, as families cultivate healthier spending habits, the ripple effects can potentially bolster the economy, laying a foundation for sustainable growth.

The Role of Policy and Regulation

Policy and regulatory frameworks also play a crucial role in shaping the financial landscape for credit card users in Canada. Historical lending practices reveal a tendency for predatory behavior during economic booms, with lenders capitalizing on consumers’ desires to maintain upward living standards. Current regulations aimed at mandating transparency in credit card agreements represent a significant stride towards enhancing consumer protection.

Moreover, proposed legislative measures to cap interest rates may also emerge as a pivotal response to consumer dissatisfaction with exploitative practices. By fostering a credit environment that prioritizes fairness and accountability, Canadians can better navigate the tumultuous waters of rising interest rates, ensuring that their financial health is not compromised as it has been in earlier economic epochs.

DISCOVER: Click here to learn how to apply for a personal loan

Conclusion

As we stand on the precipice of financial uncertainty, the historical lessons gleaned from Canada’s economic past resonate profoundly with our current challenges concerning credit card interest rates. The juxtaposition of past debt crises against today’s rising rates illustrates a recurrent cycle of consumer vulnerability exacerbated by unfettered borrowing. The alarming statistic of $1.84 for every dollar of disposable income serves as a stark reminder of the precarious position many Canadians find themselves in.

However, alongside these challenges emerges a silver lining—the burgeoning emphasis on financial literacy and proactive debt management strategies. The collective shift towards informed financial decision-making is reminiscent of past recoveries, where education and vigilance became pillars of resilience. Harnessing contemporary resources and advice, Canadians have the tools at their disposal to navigate deeply entrenched credit card debt, which has plagued households for generations.

Furthermore, the increasing discussions around policy reforms, including potential caps on credit card interest rates, indicate a growing recognition of the need for structural change that prioritizes consumer protection. By learning from previous missteps, we can advocate for a more equitable financial landscape that shields individuals from predatory lending practices.

In essence, the road ahead necessitates a concerted effort to combine education, regulation, and personal responsibility. As Canadians forge a path towards financial stability, they must draw from the lessons of the past to ensure that the weight of credit card debt does not hinder their journey to economic health and security.

Linda Carter

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on our platform. Her goal is to empower readers with practical advice and strategies for financial success.