Comparison of Tax Optimization Methods: Deduction vs. Tax Credit in the Canadian Context

Understanding Tax Deductions and Tax Credits in Canada

The evolution of tax policies in Canada has always reflected the nation’s socio-economic landscape. As governments adapt to changing fiscal climates, understanding the mechanisms of tax optimization has become crucial for individuals and businesses alike. Today, a historical perspective on tax deductions and tax credits reveals how deliberate past decisions inform contemporary practices.

Tax deductions have roots tracing back to the early tax regimes when financial relief was necessary for promoting economic growth. They function by lowering taxable income, which can be advantageous in various scenarios. For instance, business expenses such as office supplies, employee wages, and operational costs enhance the capabilities of enterprises, enabling them to reinvest in growth. The significance of such deductions can be traced to the post-World War II economic boom, which necessitated entrepreneurship to restore national economic health. Today, these deductions are critical in fostering innovation and creating job opportunities across Canada.

Another vital example is mortgage interest deductions, which play a pivotal role in easing the financial burden of homeownership. The implementation of these deductions in the 1970s recognized the need for affordable housing opportunities, encouraging families to invest in their futures and stabilize communities. By reducing the amount of taxable income through these deductions, Canadian homeowners are often able to enjoy greater financial freedom, allowing them to contribute more significantly to the economy.

Moreover, charitable contributions serve as a testament to Canada’s commitment to social welfare. Tax deductions for charitable donations have a historical precedent rooted in the post-depression era, recognizing the vital role that community support plays in national recovery. These deductions not only incentivize philanthropy but also help sustain local organizations and initiatives aimed at improving societal conditions.

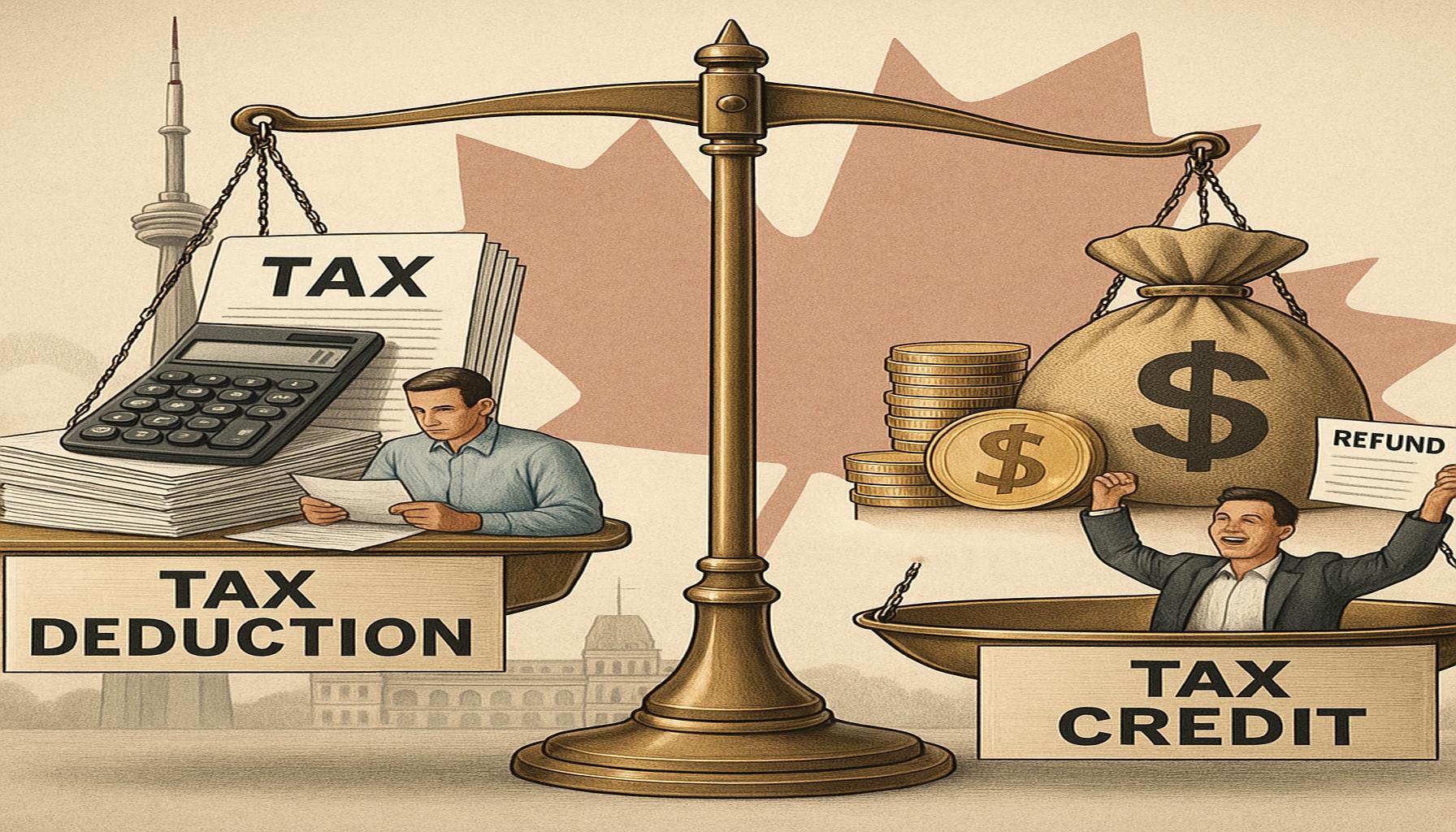

On the other hand, tax credits provide a direct reduction in tax liability and have gained increasing relevance over time. They can be categorized into non-refundable credits, which reduce taxes owed but not below zero, and refundable credits, which may result in a tax refund if the credit exceeds taxes owed. An example of a non-refundable credit is the basic personal amount, a long-standing feature designed to exempt a portion of income from taxation, a strategy introduced to alleviate financial burden and promote societal equity.

Conversely, refundable credits, such as the Canada Workers Benefit, directly support low-income workers and stimulate economic participation. The historical context of tax credits illustrates a progressive tax system that moves in tandem with societal needs while encouraging economic engagement.

By exploring these methods, we gain insights into how they serve different financial objectives. Historical lessons on tax optimization demonstrate that the choices made today will not only shape individual tax outcomes but also influence the broader economic landscape in Canada. The interplay of past and present tax policies reflects an evolving society where the quest for equitable financial relief remains paramount, underscoring the importance of informed fiscal decision-making for all Canadians.

DIVE DEEPER: Click here to learn more

Historical Perspectives on Tax Deductions in Canada

Tax deductions have played a significant role in shaping the Canadian financial landscape, especially as the country navigated periods of economic fluctuation. Fundamental to the concept of tax deductions is their ability to lower an individual’s or a business’s taxable income, thus providing immediate financial relief. This mechanism has been woven into the fabric of Canada’s tax system since its inception, reflecting the practical needs of citizens over time.

Examining the historical context of tax deductions reveals various phases where society demanded particular forms of financial assistance. For instance, the implementation of business expense deductions in the post-war years mirrored a need for economic revitalization. As businesses emerged during a time of reconstruction, allowing deductions for legitimate business costs became vital for fostering an atmosphere conducive to growth and investment. This approach not only supported individual businesses but also aimed to revitalize entire communities, bringing forth a resilience in the national economy.

Another historical cornerstone lies with the deduction for mortgage interest, introduced to encourage homeownership during the 1970s. In a nation where affordable housing was becoming increasingly elusive, this deduction recognized the aspiration of many Canadians to own their homes. By lessening the tax burden for homeowners, the government encouraged families to invest in residential properties, thereby promoting stability and development in local markets. This practice, therefore, serves as an example of how tax policy can effectively respond to social challenges and provide pathways for economic prosperity.

Furthermore, the significance of charitable contribution deductions cannot be understated. Historically emphasized during the Great Depression, these deductions reflect a societal commitment to community well-being and support for vulnerable populations. The engaging spirit of philanthropy encouraged through tax deductions allows Canadians to contribute to social causes while also enjoying noteworthy financial benefits. Today, this remains vital as communities continue to face challenges that require collective support.

The Rise of Tax Credits in the Contemporary Context

Over time, as Canada’s socio-economic needs evolved, so too did the approach to tax optimization through the introduction of tax credits. Unlike deductions, which reduce taxable income, tax credits directly decrease the amount owed in taxes. This innovative approach emerged in tandem with the government’s desire to ensure a more equitable distribution of wealth across social demographics.

Among the most significant developments in this realm are refundable and non-refundable tax credits. Non-refundable credits, such as the basic personal amount, allow taxpayers to reduce their tax burden but not surpass zero, thus enabling a foundational level of tax-free income. This illustrates a focused effort towards alleviating financial pressure on individuals, particularly those in lower-income brackets.

In contrast, refundable tax credits, which include programs like the Canada Workers Benefit, provide a more aggressive form of tax relief, enabling individuals to receive a refund if their eligible credits exceed their tax liability. This initiative was notably introduced to enhance economic participation among low-income workers, presenting a significant opportunity for social mobility. The historical trajectory of tax credits underlines an adaptive tax strategy, responding to the necessities of a diverse and evolving populace.

In conclusion, examining the interplay between tax deductions and tax credits through a historical lens reveals how each mechanism has been instrumental in shaping not only individual financial circumstances but also the broader economic landscape in Canada. Through lessons learned from past policies, Canadians can make informed decisions in optimizing their fiscal responsibilities while contributing to a more equitable society.

DISCOVER MORE: Click here to find out how to apply

The Dynamic Impact of Tax Credits on Canadian Society

As tax credits gained prominence, their implications extended beyond mere economic relief; they also served as a catalyst for change in social policy within Canada. The juxtaposition of tax credits against traditional deductions brings forth crucial insights into how governmental strategies have shifted to accommodate diverse needs, particularly during notable economic disruptions such as the 2008 financial crisis.

During times of crisis, such as the aforementioned economic downturn, refundable tax credits demonstrated their effectiveness in stabilizing the economy by providing immediate cash flow to those most affected. The Canada Emergency Response Benefit (CERB), rolled out during the COVID-19 pandemic, echoed this notion. This program not only emphasized the role of tax credits in providing swift support but also showcased how the government adapts its fiscal policies in response to emergent social needs. The rapid mobilization of such tax credits illustrated a significant lesson from previous economic trials: flexibility and responsiveness in tax policy are essential for both short-term relief and long-term recovery.

Moreover, tax credits contribute to addressing social equity by providing targeted support to marginalized groups. For instance, the disability tax credit reflects a commitment to inclusivity, designed to alleviate some of the financial burdens faced by individuals with disabilities and their caregivers. This credit illustrates how the tax system has evolved to consider the realities of different population segments, thereby fostering a sense of belonging and community support.

Additionally, education tax credits have emerged as a strategic tool for enhancing workforce development. By helping students reduce their financial burden through tax credits related to tuition fees and textbooks, the government has built pathways for more individuals to attain higher education. This approach not only benefits the individual through increased employability but also augments Canada’s skilled labor force, ultimately contributing to national economic growth. The historical precedence of investing in education reflects a consistent understanding that a well-educated populace is vital for sustained societal progress.

Comparative Efficiency of Deductions and Credits

When analyzing the comparative efficiency of tax deductions versus tax credits, it becomes apparent that the two serve different purposes within the economic fabric of Canada. While deductions, historically entrenched as fundamental mechanisms, offer advantages to higher-income individuals who can leverage them efficiently, tax credits yield more immediate relief to lower-income earners who may not benefit significantly from deductions.

This disparity raises essential questions regarding fiscal equity. As tax credits continue to evolve, their ability to reach the intended beneficiaries—often those in lower socio-economic brackets—remains a pivotal focus for policymakers. As seen with the introduction of universal tax credits, which aim to benefit all Canadians equally, there is an ongoing dialogue around how best to structure these initiatives to maximize their intended impact.

Through the lens of historical evolution, one can observe how Canada has recalibrated its fiscal approach to account for shifting demographics, economic pressures, and changing societal norms. The principles underlying tax optimization must not only be assessed through their direct financial implications but also their broader societal resonance. Accordingly, as policymakers continue to refine tax strategies, the lessons learned from historical practices in both tax deductions and credits will serve as indispensable guidance for navigating the complex landscape of taxation in the 21st century.

LEARN MORE: Click here for essential debt management strategies

Conclusion

In assessing the comparison of tax optimization methods in Canada, particularly through the lenses of deductions and tax credits, it becomes evident that each mechanism serves crucial but distinct roles within the fiscal system. Deductions, while historically entrenched, often favor higher-income earners who can maximize their benefits. In contrast, tax credits, especially in their more recent iterations, tend to provide immediate and tangible relief to lower-income families, thus bridging the gap towards greater fiscal equity.

Reflecting on Canada’s experience during economic upheavals, such as the 2008 financial crisis and the COVID-19 pandemic, we witness the profound impact of tax credits in fostering resilience and social support. Programs like CERB serve as pivotal reminders of how flexible fiscal policy can effectively address citizens’ urgent needs during tumultuous times. This responsiveness underscores the importance of adapting tax strategies that not only alleviate economic pressures but also promote social inclusivity.

As Canada moves forward, the evolution of tax credits should remain a staple in discussions around social equity, particularly concerning marginalized groups. The ongoing dialogue surrounding the effective implementation of these credits is paramount for promoting long-term financial stability in a progressively diverse society. Ultimately, the lessons learned from past fiscal strategies continue to illuminate the path forward, reminding policymakers that tax optimization is not solely about revenue generation but also about fostering a supportive and equitable economic landscape for all Canadians.